[ad_1]

Revolving accounts and installment accounts are each essential account sorts when constructing credit score, however they don’t seem to be equally highly effective relating to your credit score. Which sort of account has a better impression in your credit score rating? Maintain studying to seek out out.

Revolving Debt vs. Installment Debt: Definitions

Revolving Credit score Account Definition

A revolving credit score account is an account that permits you to “revolve” a steadiness, which suggests you shouldn’t have to pay the complete excellent steadiness on the account each month.

Revolving accounts sometimes have a credit limit as much as which you’ll be able to cost. You possibly can select how a lot to borrow from the account; you shouldn’t have to make use of the complete credit score restrict. When you make funds in opposition to the steadiness, that quantity of credit score is then accessible so that you can use once more.

Revolving accounts embrace traces of credit score and credit cards.

Installment Credit score Definition

Installment credit score, in distinction, is credit score the place the complete mortgage quantity is disbursed at one time. You then make common funds of a set quantity towards the debt over a sure time period.

Installment debt contains mortgages, auto loans, pupil loans, private loans, credit-builder loans, and every other sort of mortgage that has an everyday cost schedule of mounted funds.

How Installment and Revolving Money owed Have an effect on Your Credit score Rating

Revolving Accounts and Your Credit score Rating

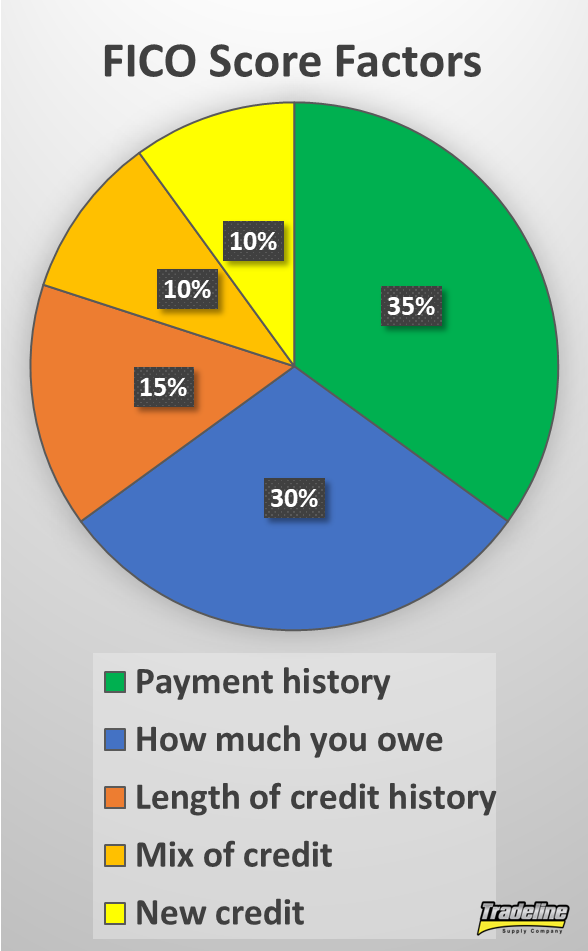

5 primary elements are thought-about by FICO scores.

As you recognize from our article on credit scores, there are 5 primary elements that affect your FICO rating:

Revolving accounts can have a major impact on every of those 5 elements.

Cost Historical past

So far as cost historical past, it’s essential to pay your payments on time each single month similar to every other account. Nevertheless, with revolving accounts, you shouldn’t have to repay the complete steadiness each month.

As an alternative, there’s probably a minimal cost quantity that you may be required to make. In case you make a cost that’s lower than the minimal cost, your account will nonetheless be thought-about delinquent.

Credit score Utilization

Loads of the ability of revolving accounts comes from their affect in your credit utilization ratios. It is because the credit score utilization issue of your credit score rating locations rather more significance on the utilization of your revolving accounts.

Having excessive revolving utilization means that you’re utilizing a big portion of your accessible credit score, which signifies to lenders that you just is perhaps at an elevated danger of default. That’s why excessive credit score utilization is dangerous information in your credit score rating.

In case you run up a steadiness on a bank card after which solely pay the minimal cost every month, you may be growing your credit score utilization. Since debt metrics resembling utilization make up 30% of your FICO rating, carrying a steadiness in your revolving accounts can significantly cut back your rating.

Size of Credit score Historical past (Credit score Age)

Credit age can be essential because it goes hand-in-hand with cost historical past. The longer you retain your revolving accounts open, the higher. Even after they’re closed, they will nonetheless proceed to age and impression your common age of accounts till they fall off of your credit score report altogether.

Customers with wonderful FICO scores have a median of seven bank cards, together with closed accounts.

Mixture of Credit score

Having a number of totally different revolving accounts can be helpful to your credit mix. Customers with FICO scores of 785 and up have a median of seven bank cards of their credit score information, together with each open and closed accounts.

Actually, in the event you don’t have sufficient revolving accounts, you will get penalized for a “lack of revolving accounts,” as a result of with out them there’s not sufficient info to evaluate your creditworthiness, according to Discover.

New Credit score/Inquiries

Having too many inquiries for revolving accounts or too many new revolving accounts can damage your credit score rating. Usually, every software for a revolving account is counted as a separate inquiry.

Installment Loans and Your Credit score Rating

Installment accounts also can have an effect on a number of the credit score rating elements, however in several methods and to totally different levels than revolving accounts do.

Cost Historical past

In terms of your credit score rating, installment loans primarily impression your cost historical past. Since installment loans are sometimes paid again over the course of some years or extra, this offers loads of alternatives to ascertain a historical past of on-time funds.

Credit score Age, Credit score Combine, and New Credit score

Since installment loans sometimes don’t rely towards your utilization ratio, you may have a excessive quantity of mortgage debt and nonetheless have good credit score.

Having not less than one installment account can be helpful to your credit mix, and installment debt also can impression your new credit score and size of credit score historical past classes.

Credit score Utilization

What installment loans don’t have an effect on, nonetheless, is your credit utilization ratio, which primarily considers revolving accounts. That’s why you may owe $500,000 on a mortgage and nonetheless have a superb credit score rating.

That is additionally why paying down installment debt doesn’t assist your credit score rating practically as a lot as paying down revolving debt.

That is the important thing to understanding why revolving accounts are a lot extra highly effective than installment accounts relating to your credit score rating. Debt metrics make up 30% of a credit score rating, and that 30% is primarily influenced by revolving accounts, not installment accounts.

Inquiries

As well as, with a FICO rating, a number of credit inquiries for sure forms of installment accounts (mortgages, pupil loans, and auto loans) will rely as only one inquiry so long as they happen inside a sure timeframe. For example, making use of for 5 bank cards can be proven as 5 inquiries in your credit score report, whereas making use of for 5 mortgage loans inside a two-week interval will solely rely as one inquiry.

Why Are Revolving and Installment Accounts Handled In another way By Credit score Scores?

Now that you recognize why revolving accounts have a extra highly effective function in your credit score rating than installment accounts, you is perhaps questioning why these two forms of accounts are thought-about in another way by credit score scoring algorithms within the first place.

In line with credit expert John Ulzheimer in The Simple Dollar, it’s as a result of revolving debt is a greater predictor of upper credit score danger. Since credit score scores are basically an indicator of somebody’s credit score danger, extra revolving debt means a decrease credit score rating.

Since revolving accounts like bank cards are often unsecured, they’re a greater indicator of how properly you may handle credit score.

Why is it that revolving debt higher predicts credit score danger than installment debt?

The primary motive is that installment loans are sometimes secured by an asset resembling your home or automobile, whereas revolving accounts are sometimes unsecured.

Because of this, you’ll be much less more likely to default on an installment mortgage, since you don’t need to lose the asset securing the mortgage (e.g. have your automobile repossessed or your private home foreclosed on).

Since revolving accounts resembling bank cards are sometimes unsecured, you usually tend to default as a result of there’s nothing the lender can take from you in the event you cease paying.

As well as, whereas installment money owed have a schedule of mounted funds that have to be paid each month, revolving money owed let you select how a lot you pay again every month (past the required minimal cost). Since you may resolve whether or not to repay your steadiness in full or carry a steadiness, revolving accounts are a greater reflection of whether or not you select to handle credit score responsibly.

How you can Use Revolving Accounts to Assist Your Credit score

Since revolving accounts are the dominant drive influencing one’s credit score, it’s smart to make use of them to your benefit somewhat than letting them trigger you to have bad credit.

Purpose to build up not less than a number of revolving accounts over time.

Right here’s what it’s essential to do to make sure your revolving accounts be just right for you as an alternative of in opposition to you:

- Make not less than the minimal cost on time, each time.

- Don’t apply for too many revolving accounts and unfold out your functions over time.

- Purpose to finally have a number of totally different revolving accounts in your credit score file.

- Maintain the utilization ratios down by paying off the steadiness in full and/or making funds greater than as soon as per thirty days. Use our revolving credit calculator to trace your utilization ratios.

- Keep away from closing bank cards in order that they will proceed to assist your credit score utilization.

Revolving Accounts vs. Installment Accounts: Abstract

- Revolving accounts are given extra weight in credit scoring algorithms as a result of they’re a greater indicator of your credit score danger.

- Revolving accounts play the first function in figuring out your credit utilization, whereas installment loans have a a lot smaller impression. Excessive utilization in your revolving accounts, due to this fact, can harm your rating.

- With a FICO rating, inquiries for installment loans are grouped collectively inside a sure timeframe, whereas inquiries for revolving accounts are usually all counted as separate inquiries. Subsequently, inquiries for revolving accounts can typically damage the “new credit score” portion of your credit score rating greater than inquiries for installment accounts.

- Use revolving accounts to assist your credit score by holding the utilization low and holding the accounts in good standing.

Credit score Skilled: Are Revolving Accounts Higher For Your Credit score Scores Than Installment Loans?

As you recognize, John Ulzheimer, who is among the prime specialists within the discipline of credit score, has contributed a number of articles to our Knowledge Center. We requested him to share his opinion on the subject of the significance of revolving credit score vs. installment credit score. General, John’s place helps our conclusions within the above article.

You possibly can learn his tackle the difficulty beneath.

Disclaimer: The next article was contributed by credit score skilled John Ulzheimer. The views and opinions expressed within the following article are these of the writer, John Ulzheimer, and don’t essentially replicate the official coverage or place of Tradeline Supply Company, LLC.

In terms of credit score scoring there are a selection of things out of your credit score studies which are scorable, which means they will presumably affect your credit score scores. Two of these objects are revolving accounts and installment loans. The query that comes up infrequently is which of those two frequent forms of credit score accounts is best in your credit scores?

What Are Revolving Accounts?

The most typical instance of a revolving account is a bank card.

“Revolving” describes one of many three forms of accounts that may seem in your credit score studies. With a revolving account, you might be assigned a line of credit score or credit limit. You possibly can draw in opposition to that line, pay it again, and draw in opposition to it once more. The most typical instance of a revolving account is a garden-variety bank card.

For instance, you probably have a credit card with a $10,000 credit score restrict you may cost as much as $10,000, pay some or all of it again, after which use some or all of that $10,000 once more. You are able to do this time and again till the cardboard issuer closes the account otherwise you select to cease utilizing that card.

When you think about the variety of banks and credit score unions on this nation, there are literally thousands of monetary establishments that difficulty bank card accounts. And, most of those bank card issuers will report your account exercise to the credit score reporting companies; Equifax, Experian, and TransUnion.

What Are Installment Loans?

“Installment” describes one other of the three forms of accounts that may seem in your credit reports. With installment accounts or loans, you will have borrowed some particular sum of money and have agreed to pay it again in mounted month-to-month funds over a set time period. A typical instance of an installment account is an auto mortgage.

For instance, in the event you borrow $30,000 to purchase a automobile you now owe the lender $30,000. You’ll be required to make the identical cost each month till the steadiness has reached zero. A typical size of time to pay again an auto mortgage is 4 years, or 48 months.

As with bank card issuers, there are additionally hundreds of monetary establishments that can prolong installment loans. Actually, most lenders supply each bank cards and installment loans. And once more, most of those lenders will report your account exercise to the credit reporting agencies.

How Do They Influence My Credit score Scores?

Though you could possibly have a whole bunch of hundreds of {dollars} of debt with a mortgage mortgage, it most likely wouldn’t have an effect on your credit score rating as a lot as your revolving debt.

Each bank cards/revolving accounts and installment loans are thought-about by the credit score scoring methods constructed by FICO and VantageScore. As such, each account sorts can affect your scores. However, they don’t affect scores equally. Not even shut.

Actually, revolving accounts have significantly extra affect in your credit score scores than installment loans. This may be counterintuitive given you may simply be in a number of hundred thousand extra {dollars} of installment debt than bank card debt (suppose residence loans versus bank cards).

Whereas installment debt can impression your credit score scores, it’s usually benign so long as you’re making your funds on time. I’ll provide you with a private instance that I’ve shared earlier than. I paid off a $250,000 mortgage mortgage by promoting my home and my scores went up on common by about 4 factors.

Now the bank card debt…ouch! A modest quantity of bank card debt could be very problematic in your credit scores, even in the event you’re making your cost on time.

Bank card debt is measured in various methods in credit scoring systems. The variety of accounts with a steadiness, the ratio of balances to credit score limits on all your open bank cards, and the identical ratio however on a card-by-card foundation. All of those metrics are very influential to your credit score scores.

If I might paint an image of a very problematic situation because it pertains to your revolving bank card debt, it could appear like this…$10,000 of bank card debt unfold equally throughout 10 totally different playing cards, every with a $1,000 credit score restrict. So principally you’d have 10 absolutely maxed-out bank cards in your credit score studies. It is a rating killer, even in the event you’re making your funds on time. So, don’t do that at residence.

The Influence of Approved Person Credit score Card Accounts

Having maxed-out bank cards in your credit score report could be disastrous in your credit score rating.

The situation I described above is a catastrophe, plain and easy. Along with having so many accounts with balances, you will have ten bank card accounts which are maxed out and, thus, are 100% utilized. The utilization ratios related together with your bank card debt are a really influential a part of your credit score scores.

Now, let’s say you opened a brand new bank card account with a $15,000 credit limit or had your title added to a bank card account as a licensed person with the identical credit score restrict, however you maintained a zero steadiness on the cardboard. If/when that account was added to your credit score studies your overall credit card utilization ratio would go from 100% to 40%.

That’s how risky your credit score scores could be simply from the way you’re managing your revolving bank card debt. Similar variety of playing cards with a steadiness. Similar quantity of combination debt. However whenever you add that new card, your utilization ratio drops. Because of this you must by no means assume you’ve bought perfect credit simply since you make your funds on time.

John Ulzheimer is a nationally acknowledged skilled on credit score reporting, credit score scoring, and id theft. He’s the President of The Ulzheimer Group and the writer of 4 books about client credit score. Previously of FICO, Equifax, and Credit score.com, John is the one acknowledged credit score skilled who really comes from the credit score business. He has 27+ years of expertise within the client credit score business, has served as a credit score skilled witness in additional than 370 lawsuits, and has been certified to testify in each Federal and State courts on the subject of client credit score. John serves as a visitor lecturer at The College of Georgia and Emory College’s Faculty of Legislation.

[ad_2]

{kind=link}